Critical and strategic minerals: what are the differences?

Introduction

The development of national lists of critical and strategic minerals has become a common practice among the major economic powers. This evolution reflects a growing attention to the structuring role that certain mineral resources play in contemporary production systems and in geopolitical balances.

These substances lie at the heart of numerous value chains, particularly in the energy, advanced technology, and infrastructure sectors. Because their production is often concentrated in a limited number of countries, their supply raises significant issues regarding economic stability and international relations.

In this context, the notions of "critical minerals" and "strategic minerals" are often used together. They do not, however, cover exactly the same issues, and distinguishing between them allows for a better understanding of the political and economic choices that underpin them.

Geographic concentration of supply as a vulnerability factor

Global demand for mineral resources is experiencing sustained growth, driven at once by energy transformations, the development of digital technologies, industrialization, and the evolution of infrastructure. This dynamic is not limited to a single sector: it reflects a more general intensification of raw material use in the world economy. In this context, the question of supply becomes a central issue.

Yet this growing demand runs up against a significant structural constraint. The production and processing of many essential mineral substances remain heavily concentrated in a small number of countries, which limits the diversification of supply sources and heightens the vulnerability of value chains.

Several recent observations help illustrate this reality:

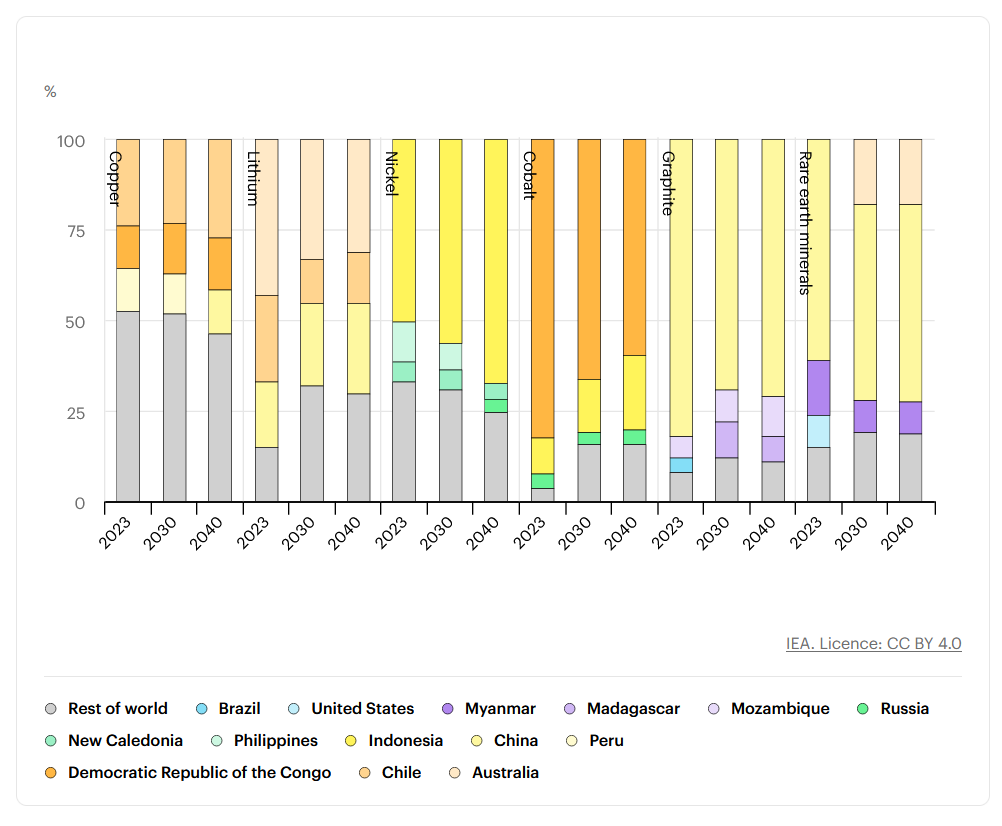

The projected growth in supply for key minerals, notably lithium, nickel, cobalt, and refined rare earths, is expected to come largely from the three leading current producers worldwide. This concentration means that the evolution of supply depends heavily on the ability of a limited number of players to increase their production [4].

In certain specific segments, the dependence is even more pronounced. This is notably the case for battery-grade spherical graphite, for which roughly 95% of supply growth is associated with China. This situation illustrates the high level of geographic specialization that characterizes certain supply chains [4].

Such concentration exposes markets to various types of risk. Disruptions may stem from geopolitical factors, environmental or social constraints, or political decisions related to the management of natural resources. The assessment of these risks therefore goes beyond the mere physical availability of materials and incorporates broader economic and institutional dimensions [7].

These levels of concentration are likely to have direct repercussions on the stability and predictability of global supply. They can notably influence costs, lead times for bringing production online, and, more broadly, the ability of industries to plan their investments over the medium and long term [4].

In this context, strengthening the resilience of supply chains has gradually established itself as a priority objective for many states and industrial players. The strategies put in place aim notably to diversify supply sources, develop local processing capacity, and encourage the recycling of materials, in order to reduce dependence on a limited number of suppliers and mitigate the associated risks.

Figure 1: World map of production concentration by country (copper, lithium, nickel, cobalt, graphite, REE) — Source: IEA, Global Critical Minerals Outlook 2024

What Is a Critical Mineral? Definition and Examples

The term "critical mineral" is the one most frequently encountered in the media and in industrial policy. It refers to a mineral substance whose economic or industrial importance is deemed high, and for which the risk of supply disruption is significant. It is important to note that this designation varies according to countries and political contexts.

Indeed, there is no universally accepted definition of what is "critical," nor any common list of the materials that should be considered as such. Methodologies vary from one country to another, but they share common challenges: economic importance, risks related to demand and supply, and dependence on dominant suppliers [7]. In the dominant discourse, this notion has mainly been used by advanced economies that possess significant industrial capacity but display gaps in their domestic production. For these countries, it designates the elements needed by their key industrial sectors but for which there are significant risks of supply disruption.

On the Quebec side, the Office québécois de la langue française defines critical and strategic minerals as a "set of substances that a given political authority considers to be critical minerals or strategic minerals, within the framework of policies related to natural resources" [2].

Criticality: a notion that evolves over time

Criticality is a key concept borrowed from supply-risk analysis. It designates the degree of importance and vulnerability associated with a given resource, and it is not fixed over time.

The criticality of a mineral substance is not solely a function of its physical availability: it also depends on changes in demand, which are determined by specific technologies and, above all, by the pace of technological development.

What is judged critical today may no longer be so in a few years, because new sources of production may appear, substitutes may be found, or technologies may evolve.

More than 60% of the substances considered critical by the United States, the European Union, Canada, and Australia are not mined in their own right: they are minor metals extracted mainly as co-products or by-products of other major minerals, that is, materials recovered incidentally during the extraction of another primary ore and therefore available in more limited volumes [7].

The Official Lists in Canada and Quebec

The notions of criticality and strategic value take concrete form through the development of official lists, established by national and provincial governments. These lists constitute guidance tools for public policy and industrial decisions. They make it possible to identify the resources deemed to be priorities based on their economic importance, the risks associated with their supply, and their role in value chains.

These exercises are not static. They rest on evolving analyses that take into account technological transformations, market needs, and geopolitical dynamics. The lists are therefore updated periodically in order to reflect current priorities and to adjust resource development strategies.

In Canada, this approach takes the form of an official list that currently brings together 34 substances of priority interest, revised in 2024 following consultations conducted with the provinces, territories, the mining industry, and Indigenous organizations [3]. This recent update illustrates the evolving nature of the notion of criticality and the attention paid to certain sectors undergoing transformation.

At the provincial level, Quebec has also defined its own list of resources deemed to be priorities. Quebec's territory stands out for the diversity of its mineral potential, which notably includes copper, graphite, niobium, zinc, cobalt, nickel, titanium, and lithium [1]. These substances play a structuring role in several industrial sectors, particularly in the fields of energy, advanced materials, and technology.

Table I : Examples of resources and their uses

| Resource | Main use |

|---|---|

| Copper | Electrical wiring, electronics |

| Graphite | Lithium-ion batteries |

| Niobium | Special steels, superconducting applications |

| Cobalt | Batteries, aerospace |

| Lithium | Energy storage, pharmaceutical applications |

| Germanium | Semiconductors, optical fibre |

| Aluminium | Transport, packaging, energy infrastructure |

| Manganese | Steel production, batteries |

| Rare earths | Permanent magnets, electronics, energy technologies |

| Zinc | Steel galvanisation, infrastructure, batteries |

| Titanium | Aerospace, lightweight alloys, industrial applications |

What Is a Strategic Mineral? And What Is the Difference?

While the label "critical" dominates in the industrial policies of importing economies, the label "strategic" takes on a different meaning depending on whether one stands on the producer's side or the user's side.

A strategic mineral is a substance whose importance is defined less by a risk of supply disruption than by its value for the national objectives of a producing country, whether those objectives are economic, industrial, or tied to national defense.

The countries that produce or extract these resources often prefer this qualifier, because these substances are of crucial importance to their economies and can potentially confer on them a position of strength as preferred suppliers to recipient countries. In certain contexts, notably in the United States, the term "strategic" refers more specifically to materials essential to the defense industry, thereby making strategic minerals a subset of critical minerals [7].

In Quebec, this notion also takes on an environmental dimension: these substances are indispensable to daily life and to the decarbonization of the provincial economy. They are essential to the manufacturing of so-called "green" technologies for producing and storing renewable energy, thereby contributing to the reduction of greenhouse gas emissions [1]. Moreover, their ability to be recycled and recovered supports the development of the circular economy, that is, an economic model that favors the reuse and recycling of materials rather than their disposal.

Also read: Which green technologies depend on critical minerals?

Two Close but Distinct Terms Depending on Position in the Supply Chain

Although there are significant overlaps between the two notions, major differences persist in the approach adopted, reflecting national priorities, the degree of industrial competitiveness, and the choice of global partners [7].

The understanding of criticality indeed varies according to the position of stakeholders in the supply chain: importing countries assess the situation from the standpoint of supply security, whereas for producing countries, the analysis incorporates a strategic dimension in addition to a risk perspective [7].

Table II : Conceptual comparison — Critical minerals vs. Strategic minerals

| Criterion | Critical mineral | Strategic mineral |

|---|---|---|

| Main perspective | Importing countries / industries | Producing countries / states |

| Dominant angle | Risk of supply disruption | National value, defense, export |

| Policy logic | Secure supply chains | Develop local resources |

A global movement

Canada has chosen not to oppose these two perspectives, but rather to integrate them into a unified approach. Thus, the Canadian critical minerals strategy, backed by nearly 4 billion dollars in Budget 2022, aims to position the country as a global supplier of choice for these resources [5]. This strategy rests on three broad orientations: economic growth, the advancement of reconciliation with Indigenous partners, and the fight against climate change [5]. These orientations reflect precisely the tension between the "critical" dimension, securing access for industry, and the "strategic" dimension, developing the national subsoil.

On the American side, the list of critical minerals published by the USGS in 2025 added 10 new substances, including copper, boron, phosphate, silicon, and uranium, owing to the vulnerabilities identified in supply chains for sectors as varied as electronics, renewable energy, steelmaking, agriculture, nuclear power, and national defense [6].

More broadly, criticality assessment exercises generally lead to the development of national strategies and lists that serve as levers for decision-makers and industrial players in their investment plans, their commercial strategies, and their participation in the global political agenda. This approach is notably adopted by Australia, Brazil, Canada, China, the European Commission, South Korea, the United States, Japan, and the United Kingdom [7].

To go further: "How are critical minerals transforming the energy sector in Canada?"

Conclusion

The distinction between "critical mineral" and "strategic mineral" is not merely a terminological nuance. It reflects different approaches depending on the position of states in supply chains and the objectives they pursue, whether that means securing access to certain resources or developing their economic and industrial potential. In practice, these two perspectives frequently overlap, particularly in jurisdictions where subsoil resources play both a domestic and an international role.

These classifications must also be understood as evolving tools. They adapt to technological transformations, market dynamics, and geopolitical balances, which explains the regular updates observed in several countries in recent years.

In this context, these resources occupy a growing place in economic and industrial strategies. They influence the structuring of value chains, guide public policy, and shape commercial relations on an international scale. As global demand evolves, their management becomes a central issue for states seeking to reconcile supply security, economic development, and energy transition [5].

Follow Squatex on LinkedIn to stay informed about developments in this rapidly evolving sector.

References

[1] Gouvernement du Québec. "Minéraux critiques et stratégiques." Quebec.ca, 2024, https://www.quebec.ca/agriculture-environnement-et-ressources-naturelles/mines/mineraux-substances-minerales/mineraux-critiques-et-strategiques.

[2] Office québécois de la langue française. "Minéraux critiques et stratégiques." Vitrine linguistique — GDT, https://vitrinelinguistique.oqlf.gouv.qc.ca/fiche-gdt/fiche/26574349/mineraux-critiques-et-strategiques.

[3] Gouvernement du Canada. "Critical Minerals — An Opportunity for Canada." Canada.ca, updated 2024, https://www.canada.ca/en/campaign/critical-minerals-in-canada/critical-minerals-an-opportunity-for-canada.html.

[4] International Energy Agency. Global Critical Minerals Outlook 2024. IEA, 2024, https://iea.blob.core.windows.net/assets/ee01701d-1d5c-4ba8-9df6-abeeac9de99a/GlobalCriticalMineralsOutlook2024.pdf.

[5] Gouvernement du Canada. "Canadian Critical Minerals Strategy." Canada.ca, 2022, https://www.canada.ca/en/campaign/critical-minerals-in-canada/canadian-critical-minerals-strategy.html.

[6] U.S. Geological Survey. "Interior Department Releases Final 2025 List of Critical Minerals." USGS.gov, 2025, https://www.usgs.gov/news/science-snippet/interior-department-releases-final-2025-list-critical-minerals.

[7] Intergovernmental Forum on Mining, Minerals, Metals and Sustainable Development. "What Makes Minerals and Metals Critical?" IGF Mining, https://www.igfmining.org/fr/resource/what-makes-minerals-and-metals-critical/.

[8] IEA (2024), Geographical distribution of mined or raw material production for key energy transition minerals in the base case, 2023-2040, IEA, Paris https://www.iea.org/data-and-statistics/charts/geographical-distribution-of-mined-or-raw-material-production-for-key-energy-transition-minerals-in-the-base-case-2023-2040-2