Which Green Technologies Depend on Critical Minerals?

Introduction

The energy transition is not just a technological revolution: it's also a mineral revolution. Rare earths, essential for wind turbine magnets, electric vehicles, and clean technologies, are seeing their demand grow at an unprecedented rate. This pressure is creating a global market reorganization, where industrial innovation and supply security are becoming inseparable. For Quebec and Canada, rich in critical minerals, this transformation represents a unique opportunity to strengthen their role in the green economy. This article examines the technologies that rely on rare earths and the prospects opened by their responsible exploitation.

Rare Earths, These 17 Elements Essential to the Energy Transition

These metals with exotic names have become the invisible pillars of our energy future. Despite their misleading name, rare earths are not that rare in the Earth's crust. What makes them precious is rather their concentration in exploitable deposits and, above all, their exceptional physical properties.

The 17 Elements of the Periodic Table

Rare earths are divided into two categories according to their atomic weight and properties: light rare earths (LREE) and heavy rare earths (HREE).

Light Rare Earths (LREE):

Lanthanum (La) – used in hybrid vehicle batteries and optical applications

Cerium (Ce) – present in catalytic converters, light bulbs, and glass polishing

Praseodymium (Pr) – employed in aircraft engines and high-performance magnets

Neodymium (Nd) – essential for industrial magnets in wind turbines and electric motors

Promethium (Pm) – radioactive element used in certain nuclear batteries

Samarium (Sm) – indispensable for high-temperature magnets and neutron absorption

Europium (Eu) – used for television screens, LEDs, and anti-counterfeiting banknotes

Gadolinium (Gd) – employed in medical imaging (MRI) and neutron shielding

Heavy Rare Earths (HREE):

Terbium (Tb) – improves magnets and serves in green phosphors for indoor lighting

Dysprosium (Dy) – increases thermal resistance of permanent magnets

Holmium (Ho) – used for nuclear reactors and powerful magnets

Erbium (Er) – employed in optical fibers and lasers

Thulium (Tm) – present in portable X-ray devices

Ytterbium (Yb) – used for seismic monitoring

Lutetium (Lu) – employed in cancer treatment and PET scanners

Scandium (Sc) – enables the use of aluminum in aerospace

Yttrium (Y) – used in superconductors, ceramics, and LEDs

Unique and Irreplaceable Properties

The magnetic, luminescent, and catalytic properties of these elements are simply irreplaceable in many technologies. For example, neodymium and dysprosium enable the creation of the world's most powerful permanent magnets, essential for compact electric motors [1]. These magnets maintain their magnetism without requiring continuous electrical power, a crucial characteristic for energy efficiency.

Green Technologies

Wind Turbines, Giants Dependent on Rare Earths

Wind energy, one of the pillars of decarbonization, relies heavily on rare earth permanent magnets. This dependence is particularly marked for offshore installations, these maritime giants that capture the powerful and constant winds of the open sea.

High-Performance Permanent Magnet Generators

Modern offshore wind turbines use permanent magnet generators containing neodymium, praseodymium, and dysprosium to improve efficiency and reduce maintenance. A large offshore wind turbine can thus contain in the order of 400 to 600 kg of rare earth-based permanent magnets, mainly neodymium and dysprosium [4][5].

Major Technological Advantages

Why use permanent magnets rather than other technologies? The advantages are considerable:

Elimination of complex gearboxes – drastic reduction in maintenance needs

Increased operational reliability – particularly crucial in hostile marine environments

Superior energy efficiency – optimal conversion of wind energy into electricity

High power density – enables more compact and powerful designs

In marine environments, where every technical intervention is extremely expensive and depends on weather conditions, this mechanical simplification becomes a major economic asset.

Variable Intensity According to Technologies

The rare earth intensity varies considerably according to wind technologies, with direct-drive turbines being the most dependent on permanent magnets. International Energy Agency studies indicate intensities of several hundred kilograms of magnets per MW installed, particularly for direct-drive offshore turbines [5].

| Wind Turbine Type | Generator Technology | Rare Earth Intensity (kg/MW) | Market Share (order of magnitude) |

|---|---|---|---|

| Direct-drive offshore | Permanent magnets (NdFeB) | ~150 to >300 kg/MW | Majority (≈70–90% of new offshore installations) |

| Direct-drive onshore | Permanent magnets (NdFeB) | ~150 to 300 kg/MW | Minority but growing (≈20–35%) |

| Onshore with gearbox | Induction or wound generator (without magnets) | Negligible to nil | Still dominant in some regions, but declining |

This significant difference explains why the technological choice of wind developers directly influences global demand for critical minerals. The trend toward more powerful turbines and offshore farms further from coasts accentuates this dependence on rare earths.

Electric Vehicles, a Revolution Hungry for Rare Earths

Every electric car on our roads contains several kilograms of strategic minerals. This reality transforms transportation electrification into a major geopolitical issue, well beyond purely environmental considerations.

Ultra-High-Performance Permanent Magnet Motors

The majority of modern electric vehicles use permanent magnet neodymium-iron-boron (NdFeB) motors to maximize range and performance. On average, an electric vehicle contains between 1 and 2 kg of permanent magnets in its motor, representing a significant amount of neodymium and sometimes dysprosium [4]. Although this quantity may seem modest, it becomes colossal when multiplied by the millions of electric vehicles expected on world roads.

The Critical Role of Dysprosium

Dysprosium plays a particularly crucial role in electric vehicle performance. This element is added to magnets to maintain their magnetic properties at high temperatures, which proves essential during intense accelerations or prolonged driving in demanding conditions.

Why is dysprosium indispensable?

Thermal stability – maintains magnetic performance up to 200°C

Resistance to demagnetization – preserves efficiency throughout the vehicle's lifetime

Range optimization – consistent energy efficiency even during intensive use

Dysprosium additions that can reach up to approximately 7% by weight, depending on the magnet grade and thermal requirements, can significantly improve the thermal stability of NdFeB magnets [7]. Without this improvement, motors would lose efficiency during intensive use, compromising the vehicle's range and performance.

Other Green Technologies Dependent on Rare Earths

Beyond wind power and electric vehicles, rare earths are omnipresent in our sustainable energy infrastructure. Their discreet but essential presence extends to areas as varied as lighting, energy storage, and hydrogen production.

Solar Systems and Motorized Trackers

In the solar sector, dependence on rare earths does not primarily concern photovoltaic modules themselves. Dominant solar panels, particularly crystalline silicon technologies, do not structurally rely on rare earths for their operation.

Dependence on critical minerals appears rather at the level of peripheral equipment, and more precisely motorized solar trackers. These tracking systems, which orient panels according to the sun's position to maximize electricity production, incorporate electric motors that may use rare earth-based permanent magnets [1].

Thus, the use of trackers allows electricity production to increase by approximately 20 to 30% compared to fixed installations, particularly in regions with high sunshine. This energy performance gain is, however, accompanied by increased dependence on critical minerals, not in photovoltaic cells, but in the electromechanical components necessary for yield optimization.

Energy Storage and Advanced Batteries

In the field of energy storage, dependence on critical minerals varies greatly depending on technologies. Lithium-ion batteries, now dominant for electric vehicles and stationary storage, rely mainly on materials such as lithium, nickel, cobalt, or graphite, which structure today's sector supply chains.

This dependence can, however, be distinguished according to major technological families:

Lithium-ion batteries

Dominant technology for electric vehicles and stationary storage, relying on key critical minerals (lithium, nickel, cobalt, graphite), without structural dependence on rare earths.Nickel-metal hydride batteries (NiMH)

Still used in some hybrid vehicles, these batteries incorporate alloys rich in lanthanum, illustrating direct dependence on rare earths. Although this technology is declining, it remains an emblematic case.Solid-state hydrogen storage

Some solutions, still at the demonstration stage or niche applications, use lanthanum-based alloys to absorb and release hydrogen reversibly. These technologies remain marginal on an industrial scale but illustrate the potential role of rare earths in advanced storage systems [3].

Catalysts for Green Hydrogen

Rare earths also play an important role in certain key stages of the hydrogen value chain. Their use does not constitute a systemic input for green hydrogen but intervenes in catalytic functions and process stabilization, particularly in production and conversion technologies.

This contribution can be distinguished according to main applications:

Water electrolysis

Some catalyst formulations and functional materials used in electrolyzers can incorporate rare earths to improve stability, conductivity, or system durability. These uses remain complementary to dominant catalytic metals but contribute to long-term performance optimization.Reforming and chemical catalysis

Cerium, notably in the form of cerium oxide (ceria), is commonly used as a catalytic promoter in reforming processes. It improves resistance to degradation, oxygen management, and overall catalyst efficiency [1].Fuel cells

In fuel cells, some rare earths are used as additives or functional material components, contributing to electrode stability, thermal management, and durability of energy conversion systems.

As the hydrogen economy develops and production volumes increase, these catalytic and functional uses could represent growing demand for rare earths, particularly for high-performance industrial applications.

LED Lighting and Energy Efficiency

LED lighting is perhaps the most widespread application of rare earths, affecting billions of devices worldwide:

Rare earths in LEDs:

Europium (Eu) – red and blue phosphors

Terbium (Tb) – green phosphors

Yttrium (Y) – host matrix for phosphors

These materials enable the high color quality and efficiency characteristic of modern LED lighting [3]. The cumulative impact of these billions of LEDs on global energy consumption reduction is considerable.

Demand in Full Explosion

Global demand for rare earths for clean energy technologies is expected to triple by 2030 compared to 2020 levels. The International Energy Agency (IEA) projects a particularly strong increase for neodymium and dysprosium used in electric vehicles and wind power [1]. This explosive growth raises crucial questions about the world's ability to secure its supply of these strategic minerals.

However, a major challenge characterizes the global supply of rare earths: the extreme geographical concentration of their production. China currently dominates the market with approximately 70% of global extraction and over 90% of refining capacity [6]. This situation creates strategic vulnerability for Western countries that depend on these materials for their energy transition.

Canada and Its Critical Minerals Strategy, a Strategic Positioning

Faced with this global dependence, Canada is deploying an ambitious strategy to secure its supply chain. This initiative, launched in 2022, recognizes that critical minerals and rare earths are not simply economic commodities but issues of national security and technological sovereignty.

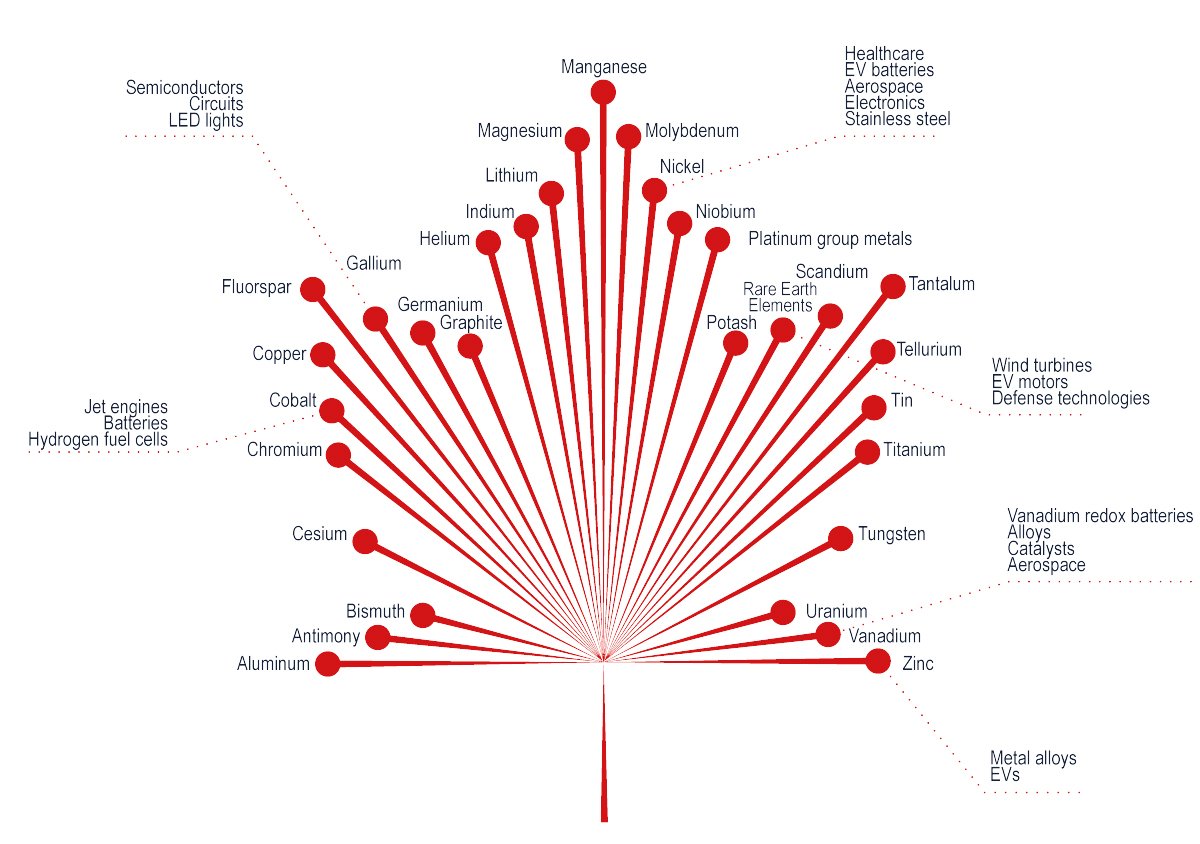

The Canadian Critical Minerals Strategy identifies 31 critical minerals, including rare earths, as essential to the country's economic security and energy transition. Among them, six are initially prioritized in this strategy for their distinct potential to stimulate Canadian economic growth and their necessity as inputs for priority supply chains [2].

Source: The Canadian Critical Minerals Strategy

The Six Strategic Pillars

Beyond resource identification, the strategy pursues six main strategic axes that frame government action:

Support exploration and development – facilitate the discovery and development of deposits

Develop processing capabilities – create refining facilities on Canadian territory

Attract foreign investment – mobilize capital necessary for large-scale projects

Strengthen international partnerships – build strategic alliances with like-minded countries

Promote clean technologies – develop responsible extraction and processing methods

Ensure Indigenous participation – guarantee the inclusion of Indigenous communities in all projects

As the Canadian government states, the objective is to make Canada a global leader in the sustainable production, processing, and recycling of critical minerals [2].

Conclusion

The green technologies that will shape the energy future rest on an often underestimated reality: the energy transition is also a mineral transition. From offshore wind turbines incorporating several hundred kilograms of rare earth-based permanent magnets to electric vehicles equipped with high magnetic efficiency motors, critical minerals have become indispensable inputs for the decarbonization of energy systems.

This growing dependence raises structural challenges: development of processing capacities, supply chain security, reduction of environmental impacts, and strengthening social acceptability of projects. At the same time, it opens significant prospects for territories capable of combining geological potential, technical expertise, and high environmental standards. It is in this context that Ressources et Énergie Squatex is interested in the critical minerals sector as a strategic lever complementary to the energy transition.

To follow Squatex's reflections, analyses, and projects around resources essential to the energy transition, follow us on LinkedIn.

References

[1] International Energy Agency. "Critical Minerals Data Explorer." IEA, 2024, www.iea.org/data-and-statistics/data-tools/critical-minerals-data-explorer.

[2] Government of Canada. "The Canadian Critical Minerals Strategy." Natural Resources Canada, 2022, www.canada.ca/en/campaign/critical-minerals-in-canada/canadian-critical-minerals-strategy.html.

[3] International Energy Agency. Global Critical Minerals Outlook 2025. IEA Publications.

[4] EWI. Rare Earth Materials – Major Industrial Uses. Technical data on typical mass of NdFeB magnets in wind turbine generators.

[5] International Energy Agency. The Role of Critical Minerals in Clean Energy Transitions, 2021 — rare earth intensity data per MW.

[6] Mining Technology. China currently controls over 69% of global rare earth production, 2025 - https://www.mining-technology.com/analyst-comment/china-global-rare-earth-production.

[7] Zhou, Bowen, et al. "Recent Progress in High-Performance Nd–Fe–B Permanent Magnets." Rare Metals, vol. 35, no. 8, 2016, pp. 601–609. ScienceDirect, https://www.sciencedirect.com/science/article/pii/S2214993716300641